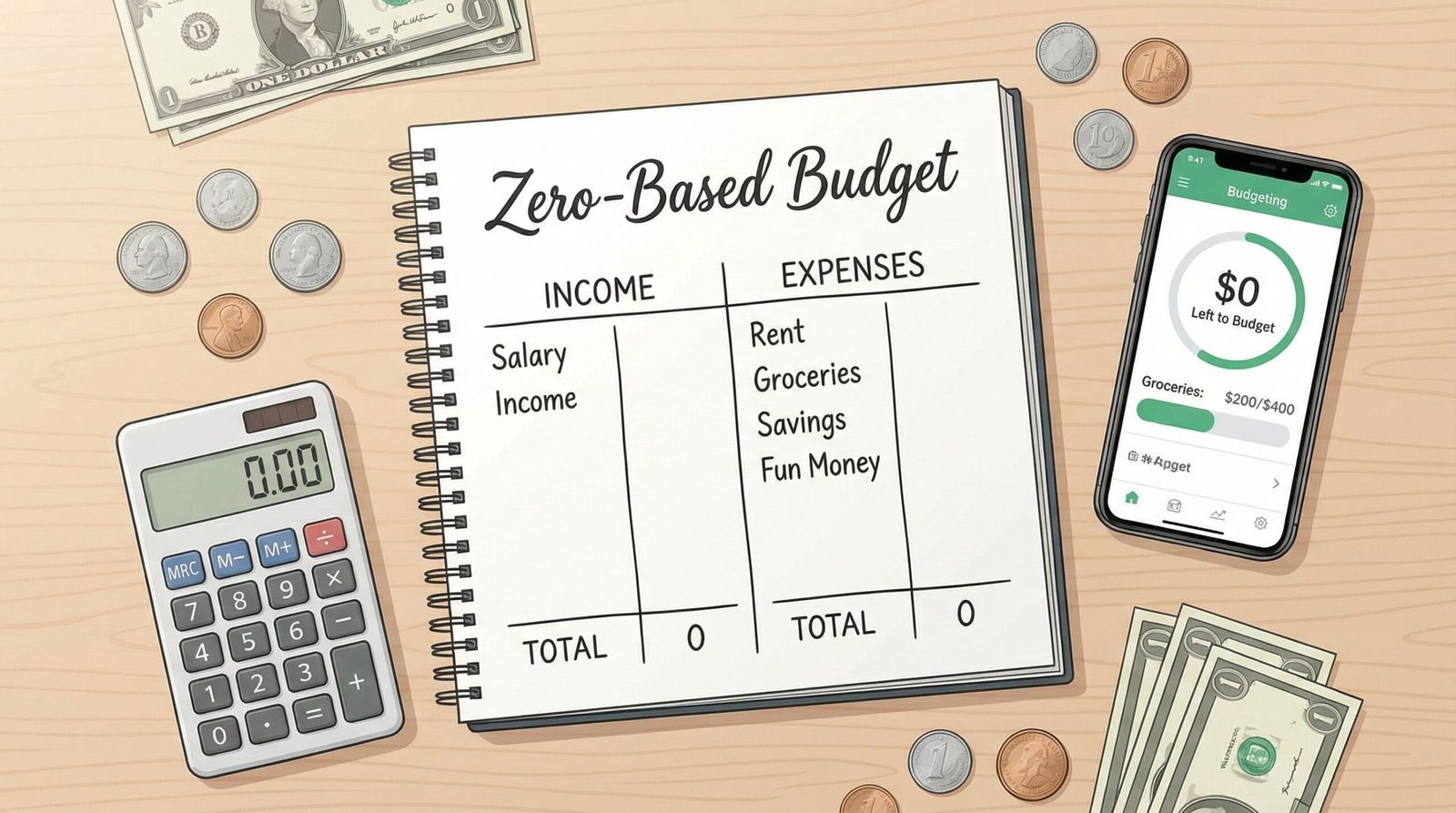

Zero-based budgeting is a budgeting method where income minus expenses equals 0 by assigning every dollar to a specific category. This method helps beginners understand exactly where money goes and prevents unplanned spending.

- Zero-based budgeting assigns every dollar a clear purpose.

- Zero-based budgeting improves spending awareness and control.

- Zero-based budgeting works best with monthly planning and tracking.

1. What Is Zero-Based Budgeting?

Zero-based budgeting is a system that requires every unit of income to be assigned to spending, saving, or debt categories until no money remains unplanned. Zero-based budgeting does not mean spending everything. Zero-based budgeting means giving each dollar a job.

Zero-based budgeting originated in business finance and later became popular in personal finance education. The method focuses on awareness, control, and intentional money management.

This budgeting approach works especially well for beginners who struggle to track spending or save consistently.

2. How Zero-Based Budgeting Works

Zero-based budgeting works by matching total income with planned expenses, savings, and financial goals so the balance reaches 0.

Step-by-step process

- List total monthly income.

- List fixed expenses.

- List variable expenses.

- Assign savings and debt payments.

- Adjust categories until balance equals 0.

Each step ensures clarity. No money remains unassigned.

| Category | Amount |

|---|---|

| Income | 2000 |

| Rent | 700 |

| Food | 350 |

| Transport | 150 |

| Savings | 300 |

| Debt | 200 |

| Entertainment | 300 |

| Total Remaining | 0 |

This example shows how every dollar receives a purpose.

3. Why Zero-Based Budgeting Is Effective

Zero-based budgeting is effective because it removes guesswork and forces intentional financial decisions.

- Improves spending awareness.

- Reduces impulse purchases.

- Encourages savings discipline.

- Supports debt reduction planning.

People who follow structured budgeting methods often experience improved financial confidence. According to the U.S. Consumer Financial Protection Bureau, budgeting improves financial stability and decision-making (CFPB).

4. Zero-Based Budget vs Other Budgeting Methods

Zero-based budgeting differs from other methods because it assigns every dollar instead of using percentage rules.

| Method | Core Rule |

|---|---|

| Zero-Based Budget | Income minus expenses equals 0 |

| 50/30/20 Rule | Fixed percentage allocation |

| Envelope System | Cash-based category limits |

Beginners can explore alternative methods in this guide: Simple Budgeting Methods That Actually Work.

5. Who Should Use Zero-Based Budgeting?

Zero-based budgeting suits beginners, families, freelancers, and individuals with irregular income.

This method works well for people who want full control of monthly finances.

Individuals struggling to separate essential expenses from non-essential expenses can benefit from learning needs vs wants before applying this method.

6. Common Mistakes in Zero-Based Budgeting

Zero-based budgeting fails when users ignore tracking and category adjustments.

- Underestimating variable expenses.

- Skipping savings categories.

- Not updating budgets monthly.

- Using unrealistic numbers.

Monthly reviews prevent these mistakes.

7. How to Track a Zero-Based Budget

Zero-based budgeting tracking requires regular expense recording and category comparison.

Tracking options

- Spreadsheet templates.

- Mobile budgeting apps.

- Printable planners.

You can explore free tools here: Best Free Budgeting Tools for Beginners.

8. Zero-Based Budget for Savings and Debt

Zero-based budgeting supports savings and debt by assigning fixed monthly targets.

Savings categories may include emergency funds, education funds, or retirement accounts. Debt categories may include credit cards, personal loans, or student loans.

The Federal Reserve emphasizes consistent savings habits as a foundation for financial security (Federal Reserve).

9. Zero-Based Budget with Extra Income

Zero-based budgeting includes side income by reallocating new income categories.

People earning additional income through freelance work or online services should assign this income carefully. Learn more about income opportunities in this guide: What Is a Side Hustle.

10. How Zero-Based Budget Improves Money Habits

Zero-based budgeting builds strong daily money habits through structured planning.

Daily habits such as expense logging and category review improve long-term financial health. You can explore helpful routines here: Daily Money Habits.

11. Zero-Based Budget and Financial Planning

Zero-based budgeting supports financial planning by aligning income with future goals.

Financial planning involves saving, investing, and protecting money over time. Learn more about planning concepts here: What Is Financial Planning.

12. Monthly Budget Setup with Zero-Based Method

Zero-based budgeting requires monthly setup to reflect changing income and expenses.

Beginners can follow this detailed monthly guide: How to Create a Monthly Budget.

13. Advantages and Disadvantages

Zero-based budgeting offers control but requires discipline.

| Advantages | Disadvantages |

|---|---|

| Clear money control | Time-consuming |

| Improved awareness | Requires tracking |

| Better savings habits | Needs monthly updates |

Conclusion

Zero-based budgeting offers beginners a practical and structured method to manage income responsibly. This budgeting system improves awareness, reduces waste, and supports long-term financial goals when used consistently.

Frequently Asked Questions

Yes or No: Is zero-based budgeting good for beginners?

Yes, zero-based budgeting is suitable for beginners because it provides clear structure and spending control.

Yes or No: Does zero-based budgeting require spending all income?

No, zero-based budgeting requires assigning income, including savings and debt payments.

Yes or No: Can zero-based budgeting work with irregular income?

Yes, zero-based budgeting works with irregular income by adjusting categories monthly.

Yes or No: Is zero-based budgeting better than percentage methods?

No, zero-based budgeting depends on personal preference and financial discipline.

Yes or No: Does zero-based budgeting reduce debt faster?

Yes, zero-based budgeting improves debt control through fixed payment planning.