Needs are essential expenses required for daily living, while wants are optional purchases that improve comfort or enjoyment. Understanding this difference allows better spending control, improved budgeting accuracy, and stronger long-term financial habits.

Key Takeaways:

- Needs are essential expenses required for basic living.

- Wants are optional purchases that improve comfort or enjoyment.

- Separating needs from wants helps control spending decisions.

- Simple tracking methods improve financial awareness.

- Clear priorities support long-term financial stability.

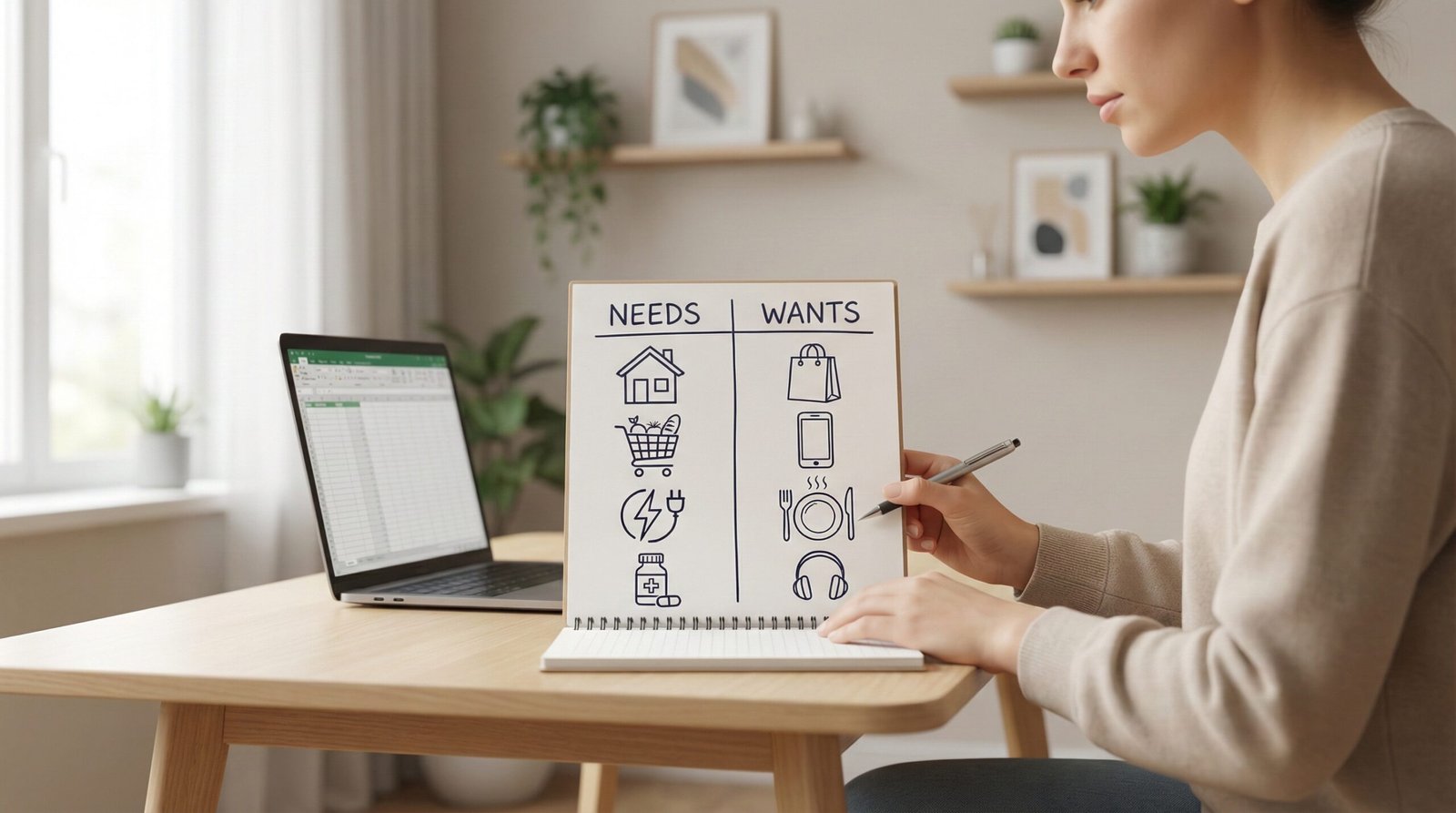

1. What Are Needs in Personal Finance?

Needs are expenses required to maintain basic health, safety, and daily functioning. Needs include costs that cannot be realistically avoided without risking financial or physical harm.

Common examples of needs include housing rent, electricity bills, basic groceries, transportation for work, essential clothing, insurance premiums, and healthcare expenses. These costs exist regardless of lifestyle choices.

Needs remain relatively stable over time. Although amounts can vary, needs must always be covered before allocating money to non-essential categories.

Examples of Needs

- Monthly rent or home mortgage

- Utility bills such as electricity and water

- Basic food supplies

- Transportation fuel or transit passes

- Medical care and insurance

Needs create the foundation of any financial plan. Budgeting without prioritizing needs leads to unstable money management.

2. What Are Wants in Personal Finance?

Wants are non-essential purchases that improve lifestyle comfort or enjoyment. Wants can be delayed, reduced, or removed without affecting basic survival.

Wants include entertainment subscriptions, restaurant dining, upgraded gadgets, branded clothing, and travel experiences. Wants reflect personal preferences rather than survival requirements.

Wants change more frequently than needs. Marketing, social trends, and emotions influence spending decisions in this category.

Examples of Wants

- Streaming subscriptions

- Restaurant meals

- Gaming accessories

- Luxury clothing brands

- Recreational travel

Wants are not harmful. However, uncontrolled spending in this category causes budget imbalance.

3. Why Separating Needs and Wants Controls Spending

Separating needs and wants improves spending awareness and reduces impulse purchases. Clear categorization allows better financial decision-making.

When expenses are grouped correctly, financial priorities become visible. This visibility helps identify overspending areas and supports realistic adjustments.

Financial education authorities recommend structured budgeting systems for improved control. The Consumer Financial Protection Bureau provides official budgeting guidance at https://www.consumerfinance.gov/consumer-tools/budgeting/.

| Category | Purpose | Control Level |

|---|---|---|

| Needs | Survival and stability | Low flexibility |

| Wants | Comfort and enjoyment | High flexibility |

This separation supports budgeting methods such as percentage-based budgeting and zero-based budgeting.

Readers who want structured budgeting support can explore monthly budgeting guidance for beginners for step-by-step implementation.

4. How to Identify Needs vs Wants in Real Life

Needs are expenses required to maintain income, health, and safety, while wants are expenses that improve convenience or pleasure.

Decision Checklist

- Is the expense required for employment?

- Is the expense required for health or safety?

- Can the expense be delayed without harm?

- Does the expense provide optional comfort?

If the answer is yes to safety or income questions, the cost belongs to needs. If the expense can be postponed without consequences, the cost belongs to wants.

Financial educators from Harvard Extension School highlight basic money priorities at https://extension.harvard.edu/blog/5-personal-finance-basics/.

5. How to Control Spending Using Needs and Wants

Spending control improves when needs are funded first and wants receive fixed limits.

Practical Steps

- Track all expenses for 30 days

- Label each expense as need or want

- Set spending limits for wants

- Review spending weekly

- Adjust limits monthly

Free tools can simplify tracking. Beginners can explore free budgeting tools to organize expenses efficiently.

Daily financial discipline improves results. Readers can learn supporting habits from daily money habits.

6. Needs vs Wants in Budget Percentages

Needs typically consume 50% to 60% of income, while wants should remain below 30%.

This distribution aligns with common budgeting models. Remaining income supports savings and financial goals.

| Income Portion | Category |

|---|---|

| 50% – 60% | Needs |

| 20% – 30% | Wants |

| 10% – 20% | Savings |

Saving guidance can be found in simple saving methods.

7. Common Mistakes When Classifying Expenses

Mislabeling comfort expenses as needs increases overspending risk.

Frequent Errors

- Calling premium internet a need

- Calling dining out a need

- Calling entertainment subscriptions a need

- Ignoring savings as a priority

Correct classification supports accurate financial planning. Beginners can review money management fundamentals for structured learning.

8. Needs vs Wants for Financial Goals

Clear expense classification improves goal achievement timelines.

Financial planning improves when unnecessary expenses decrease. Official IRS guidance on financial stability is available at https://www.irs.gov/individuals/financial-security.

Goal-focused planning concepts are explained in financial planning fundamentals.

9. Needs vs Wants for Extra Income Decisions

Understanding expense priorities reduces pressure to increase income unnecessarily.

When spending improves, financial stress decreases. Extra income remains useful, but not mandatory for stability. Readers interested in income growth can learn about side hustle basics.

Conclusion

Needs and wants classification is a core personal finance skill. Needs protect stability. Wants improve lifestyle. Balanced spending builds financial confidence, reduces stress, and supports long-term planning.

Frequently Asked Questions

Is rent always a need?

Yes, rent is a need because housing is essential for safety and stability.

Is eating at restaurants a want?

Yes, restaurant dining is a want because home-prepared meals can meet nutritional needs.

Can internet service be a need?

Yes, internet service can be a need when required for work or education.

Is saving money a need?

Yes, saving money is a need because financial protection supports long-term stability.

Are subscriptions always wants?

Yes, most subscriptions are wants unless required for employment or education.