Starting financial planning with limited income involves tracking every dollar, prioritizing essential expenses, and systematically reducing debt to create surplus cash flow. Many people believe that wealth management is only for the wealthy, but the discipline of planning is actually more critical when resources are scarce. A strategic approach ensures that every paycheck contributes toward immediate stability and future growth, preventing minor setbacks from becoming major financial crises.

- Financial planning focuses on managing existing cash flow effectively, regardless of income level.

- Zero-based budgeting helps identify wasteful spending and redirects funds to savings.

- Building a small emergency fund prevents high-interest debt from accumulating during unexpected events.

1. Assess Your Current Financial Reality

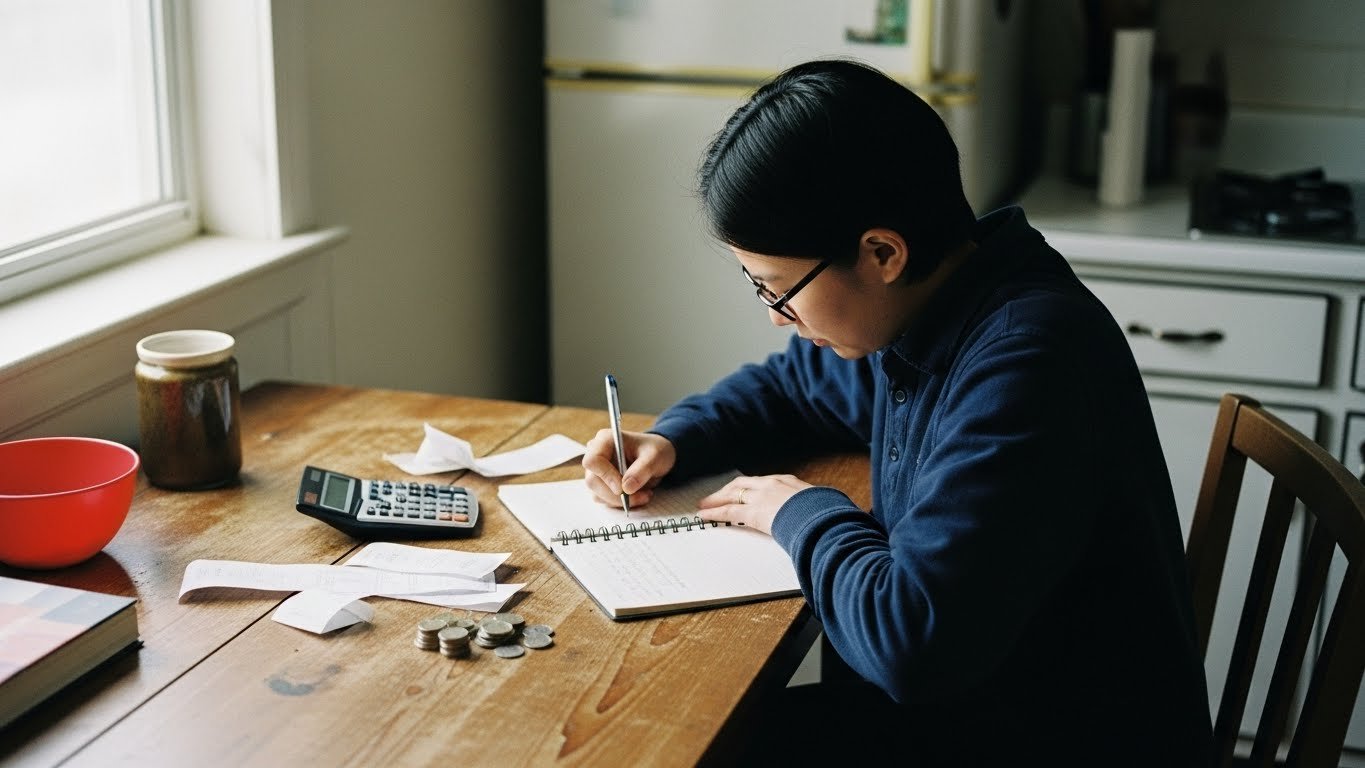

The first step in financial planning is to document your total income, all monthly expenses, and total debt obligations to understand your net cash flow. You cannot improve what you do not measure. This assessment provides the data necessary to make informed decisions about where to cut costs.

Begin by gathering bank statements, pay stubs, and credit card bills from the last 3 months. List every source of income and every outgoing payment. This process often reveals “spending leaks”—small, recurring expenses that drain your wallet without you noticing. Once you have the numbers, you can determine if you are spending more than you earn, a situation known as a deficit. Fixing this deficit is the priority before investing can begin. To get the basics right, you should learn how to create a monthly budget for beginners.

2. Choose a Strict Budgeting Method

A zero-based budget is the most effective method for limited incomes because it assigns a specific purpose to every dollar before the month begins. Unlike flexible budgeting methods, zero-based budgeting ensures that income minus expenses equals zero. This does not mean you have zero dollars left in your bank account; it means every dollar has a job, whether that is paying rent, buying groceries, or moving into a savings account.

When funds are tight, general estimations lead to overdrafts. By allocating funds precisely, you prevent overspending in non-essential categories. If you have an irregular salary, such as freelance work or hourly shifts, this method adapts well because you budget only what you have received. For a deeper understanding of this technique, read about the zero-based budget explained simply for beginners.

3. Distinguish Needs From Wants

Financial planning on a low income requires strictly categorizing expenses into essential survival needs and discretionary wants. Needs include housing, utilities, basic groceries, and transportation to work. Wants include dining out, subscription services, and brand-name clothing. When money is limited, the “wants” category often must be paused temporarily to fund financial stability.

The Consumer.gov guide on making a budget suggests that housing should ideally cost no more than 30% of your gross income, though this is difficult in high-cost areas. If your needs exceed your income, you must look for structural changes, such as finding a roommate or moving to a cheaper apartment, rather than just cutting coupons. This discipline is essential for long-term success.

4. Build a Micro-Emergency Fund

A micro-emergency fund is a savings buffer of 500 to 1,000 dollars designed to cover minor unexpected costs without using credit cards. While experts often recommend saving 3 to 6 months of expenses, that target can feel impossible when starting with little money. A smaller, achievable target provides immediate psychological relief and financial protection.

Unexpected events like a flat tire or a medical copay can derail a tight budget. Without cash on hand, you might rely on high-interest credit cards or payday loans, which trap you in a cycle of debt. Keep this money in a separate savings account so it is not accidentally spent on daily purchases. Once you clear your high-interest debt, you can expand this fund to cover full living expenses.

5. Establish Clear Financial Goals

Setting specific, measurable financial goals helps you allocate limited resources toward what matters most, distinguishing between immediate desires and future security. Without clear targets, it is easy to lose motivation when the budget feels restrictive. You need to know exactly what you are sacrificing for.

Goals should vary in timeframe. A short-term goal might be paying off a 500 dollar credit card balance within 3 months. A long-term goal might be saving 5,000 dollars for a down payment on a car over 2 years. Writing these down makes them tangible. To understand how to balance these different timelines, review the guide on short-term vs long-term financial goals explained.

6. Create a Debt Repayment Strategy

The debt avalanche method is the mathematically fastest way to become debt-free by targeting the balance with the highest interest rate first. High-interest debt acts as an anchor, holding back your ability to build wealth. By paying off the loan with the highest rate, you reduce the total amount of interest paid over time.

Alternatively, the debt snowball method focuses on paying the smallest balance first. This provides quick wins and psychological momentum, which can be crucial when you feel discouraged by limited income. Choose the strategy that keeps you motivated, but commit to applying any extra found money toward these payments.

7. Utilize Free Financial Tools

Free budgeting apps and financial calculators automate the tracking process and reduce the mental load of managing complex finances. You do not need expensive software or a financial advisor to get organized. Many free tools connect to your bank accounts to categorize transactions automatically.

These tools can generate reports showing exactly what percentage of your income goes to food, housing, or debt. This visual data is powerful. It forces you to confront spending habits that might otherwise go unnoticed. The U.S. Securities and Exchange Commission (SEC) offers excellent free calculators to help you project how small savings can grow over time.

8. Increase Your Income Streams

Increasing your income through side hustles or upskilling is often necessary when cost-cutting measures can no longer squeeze more value from your existing paycheck. There is a mathematical limit to how much you can save, but there is no theoretical limit to how much you can earn. Even an extra 200 dollars a month can significantly impact a tight budget.

Consider gig economy jobs, freelance writing, or selling unused items online. Use the extra income strictly for your financial goals—like filling that emergency fund or paying off debt—rather than lifestyle inflation. This temporary hustle can accelerate your journey to financial stability significantly.

Comparison of Budgeting Methods for Low Income

Choosing the right framework is critical when your margin for error is small. Here is how common methods compare for those with limited funds.

| Method | Structure | Best For | Low Income Suitability |

|---|---|---|---|

| Zero-Based Budgeting | Income – Expenses = $0 | Detail-oriented planners | High: Prevents waste effectively. |

| Envelope System | Cash only for variable costs | Overspenders | High: Physically limits spending. |

| 50/30/20 Rule | 50% Needs, 30% Wants, 20% Savings | General guidance | Low: Needs often exceed 50% on low income. |

| Pay-Yourself-First | Save first, spend the rest | Automated savers | Medium: Requires consistent surplus. |

Conclusion

Financial planning with limited income is not about restricting your life; it is about taking control of your resources to build a safer future. By assessing your reality, choosing a strict budgeting method like zero-based budgeting, and building a micro-emergency fund, you create a foundation that can withstand economic shocks. Start small, be consistent, and focus on incremental progress. The path to financial freedom begins with the management of the money you have today.

Frequently Asked Questions

Can I start investing with very little money?

Yes, you can start investing with as little as 5 or 10 dollars using fractional share trading platforms and micro-investing apps. These platforms allow you to buy portions of expensive stocks, making the market accessible to everyone.

What is the first thing I should do if I live paycheck to paycheck?

Yes, the absolute first step is to track your spending for one month to identify exactly where your money goes. Once you have visibility, you can cut non-essential expenses to build a small cash buffer.

Should I save money or pay off debt first?

Yes, you should save a small emergency fund of roughly 1,000 dollars first, then focus aggressively on high-interest debt. This small fund prevents you from going back into debt when a minor emergency occurs.

Is financial planning worth it for low-income earners?

Yes, financial planning is arguably more important for low-income earners because the margin for error is smaller. Proper planning maximizes the utility of every dollar and provides a roadmap out of financial hardship.

How do I budget if my income changes every month?

Yes, you should use the “lowest month” strategy where you budget based on your lowest expected income. If you earn more in a given month, the extra money should immediately go toward savings or debt reduction.